Did games really get more costly to make?

By how much, since when, and for whom? We have the receipts.

Long time no see! You might have noticed we went quiet for a few months. The enthusiasm around our first articles caught us off guard! We took that time to go full-time on Hushcrasher, plug in new data sources, set up the company properly, and sketch out a few tools we think devs and publishers will need. Buckle up, we’re back!

“Development budgets have skyrocketed.” So the story goes. Everyone nods along.

But what does that actually mean? Did budgets really skyrocket, across every scope and genre? By how much? Since when? Does it hit solodevs the same way it hits AAAs?

In a previous post, we explained how we built a model to estimate the budget of all games on Steam (if you needed a reason to trust those estimates, Jason Schreier has since reported real figures that fall right in line with ours).

What follows is our attempt to put real numbers behind the rumors. Our 2026 and 2027 forecasts are at the end.

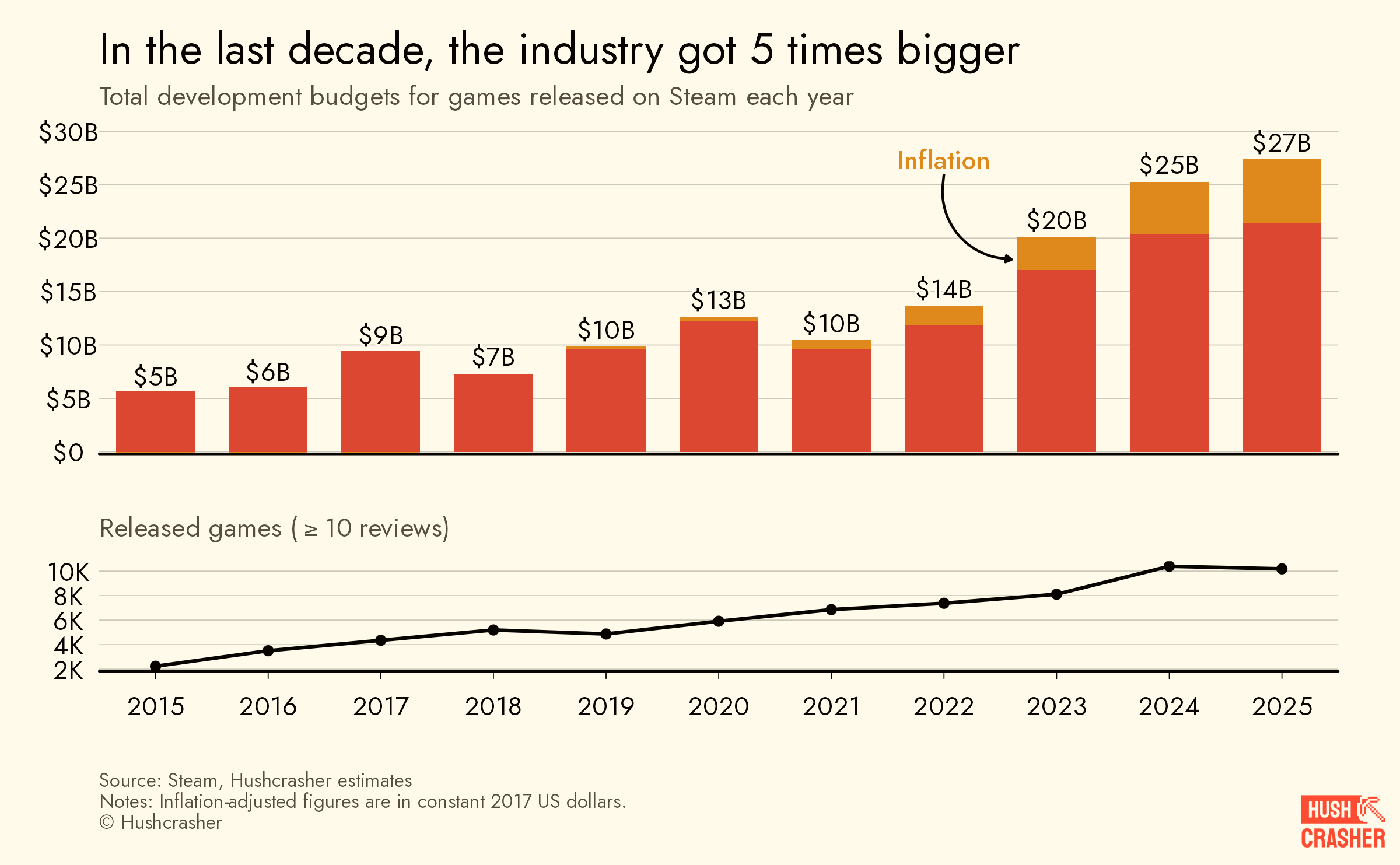

$27B spent on developing games in 2025

The video game industry has never been so big. The cumulated budgets of every games released on Steam in 2025 sum up to an all-time record of $27 billion. That’s five times what it was a decade ago, and x2.7 what is was in 2019 (x2.2 after adjusting for inflation).

For perspective: total spending on feature films and series in 2025 sits just above $40 billion. This means PC game budgets alone are the equivalent of 67% of the entire filmed fiction market.

A growth that big has two potential drivers: more games are made, or games are costlier. The number of releases doubled between 2019 and 2025. The likely reason is the surge in a new generation of solo developers during the COVID era. If they started during lockdown, a first wave of shipped games would have landed in 2021-2022.

So, volume alone explains a lot, but not all of it. Are individual games getting more expensive to make?

Stonks

When you look at the average budget per game, the same increase holds. Between 2019 and 2025, the average development cost almost doubled. Without inflation, 2025 budgets would have been 28% lower.

Costs started climbing sharply from 2022 onward, boosted by inflation. This aligns well with the first games doped by the large post-covid investment and a 2-3 years development cycle lag.

So here you know: budgets are genuinely rising and not just because of inflation.

Still, as the volume of Kei/solodevs games exploded in the last decade, looking at the market average is pretty much like watching the evolution of solodevs. Each scope level might have very different patterns.

This is part of our Budget series, breaking down the costs of making games.

Harder, Bitter, Longer, Costlier

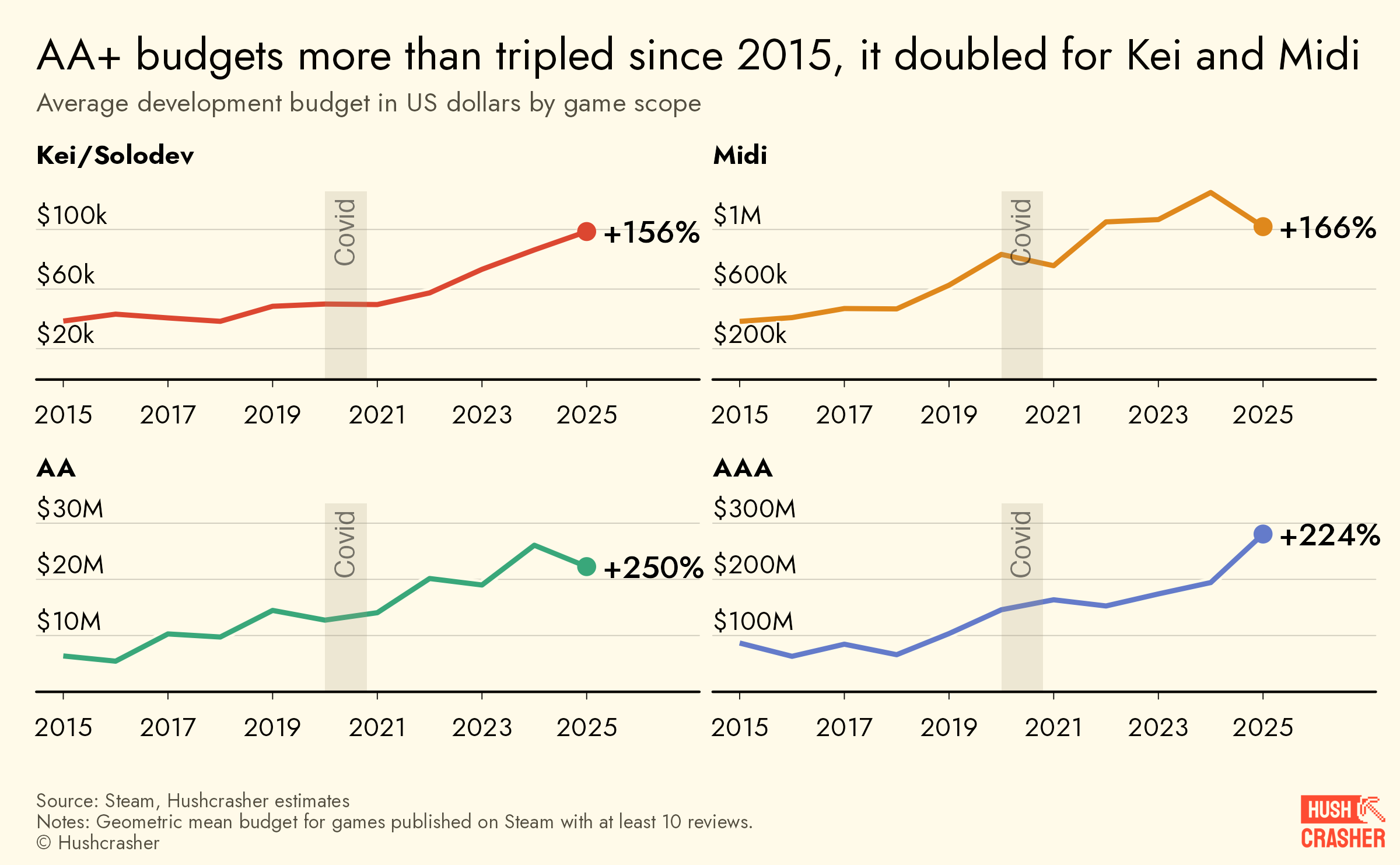

Across all scopes, games are more expensive to make. And the bigger the scope, the higher the rise. AA & AAA budgets tripled in the last decade, while smaller scopes still hit a respectable x2.5. The general figure is clear, still some interesting details are worth noting.

If “Kei” and “Midi” don’t ring a bell, we defined four data-driven categories of game scope in a previous article: Kei (solodev-scale), Midi (small studios), AA, and AAA.

Kei budgets were essentially flat until 2021, then doubled in four years.

Midi and AA both show a correction in 2025, after years of steady increases. The general trend remains the same, though.

As for AAA, the jump in budgets is gigantic in absolute terms: from ~$100M in 2019 to nearly $300M in 2025. We’re now talking about AAAs that rival the Cook Islands’ GDP!

Here’s our take on this global increase, beyond the usual “labor costs got higher” explanation. As the video game industry becomes more of a winner-takes-all market, every studio competes for the same finite resource: player’s attention. One title captures it, the rest are forgotten. This wasn’t always that potent: console exclusives used to scatter competition across separate submarkets; marketing depended on local diffusion (journalists, print magazines, retail stores). That fragmentation created room for multiple winners. Today, the market is converging toward a single arena (Nintendo being the stubborn exception).

The increased competition makes every game fight to be the one left standing. But not every studio fights the same war. Small-scope games and big-scope ones differentiate in completely different ways, and that’s what explains the budget gap.

Lower-scope games differentiate horizontally (original mechanics, unusual art, untapped themes). Doing so, it’s like they’re creating their own niche (partially escaping the competition) while not having to spend that much more. Think Disco Elysium, or Return of the Obra Dinn.

Meanwhile, AA & AAA differentiate vertically: more content, more realism, more skins, more of everything, in an unstoppable quality ladder. So any efficiency gain (better engines, AI pipelines) doesn’t translate into cheaper games. It makes them more ambitious and expensive. The result is an arms race where spending explodes.

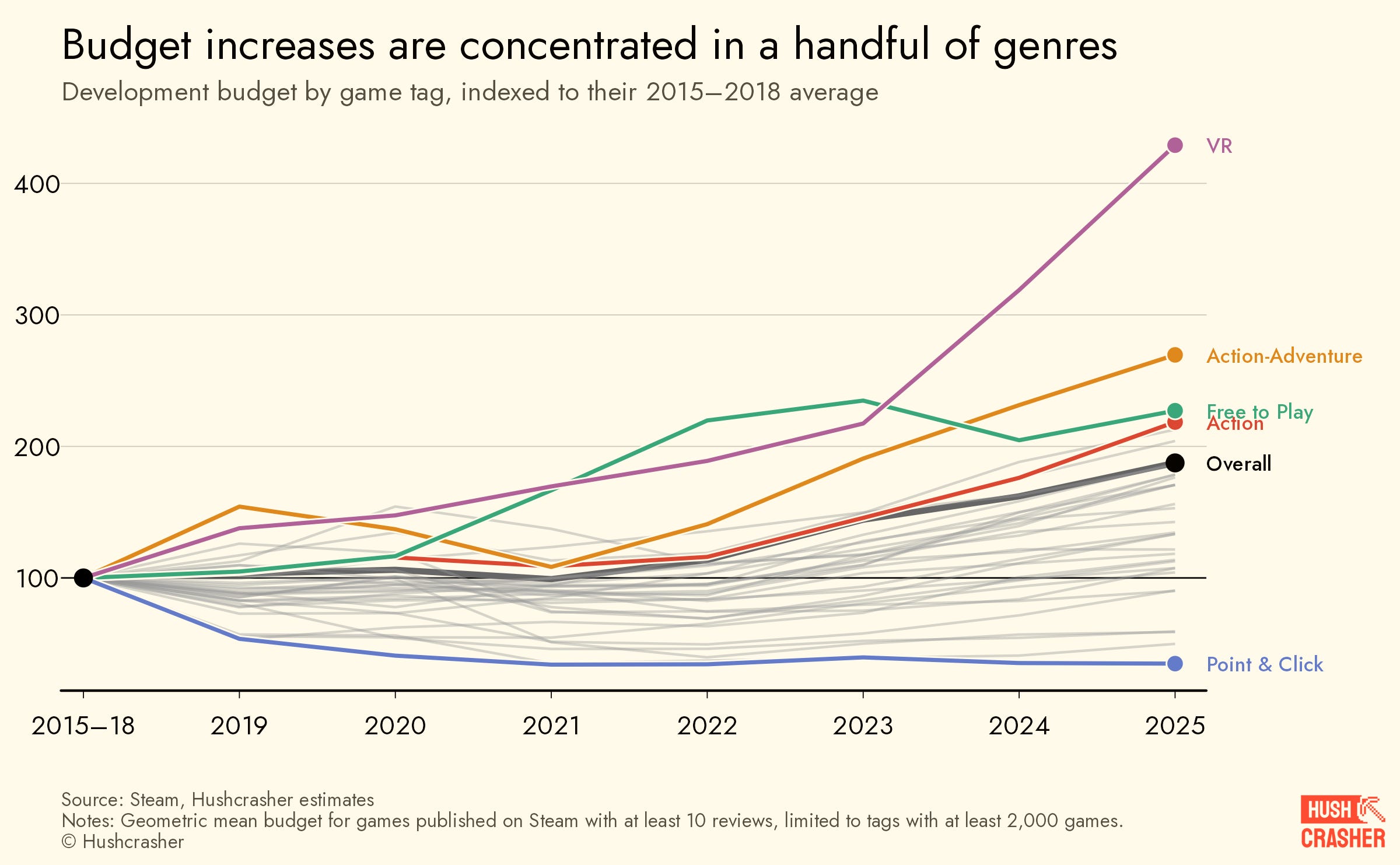

Virtual Reality, Real Costs

VR costs top the chart with a x4.3 increase in seven years. Budgets were flat until 2021, then exploded. Likely due to the 2021–2022 VC wave and metaverse hype that finally landed games in 2024. This is probably not driven by popularity, but by the mix of technical cost of building convincing virtual worlds, and the expected gold rush. Leaving reality is not cheap.

Action-Adventure (×2.8) and Free to Play (×2.3) escalated for a different reason. These are among the most popular genres, and as expected, when competition grows fierce, you need to spend more to get attention.

Point & Click, at the other end, has gotten cheaper. It’s now a genre made by small teams who’ve found ways to do more with less, or simply decided to do less. Not every budget was doomed to point skyward.

In short, budget increases have concentrated mainly on the most popular genres, where competition is the fiercest.

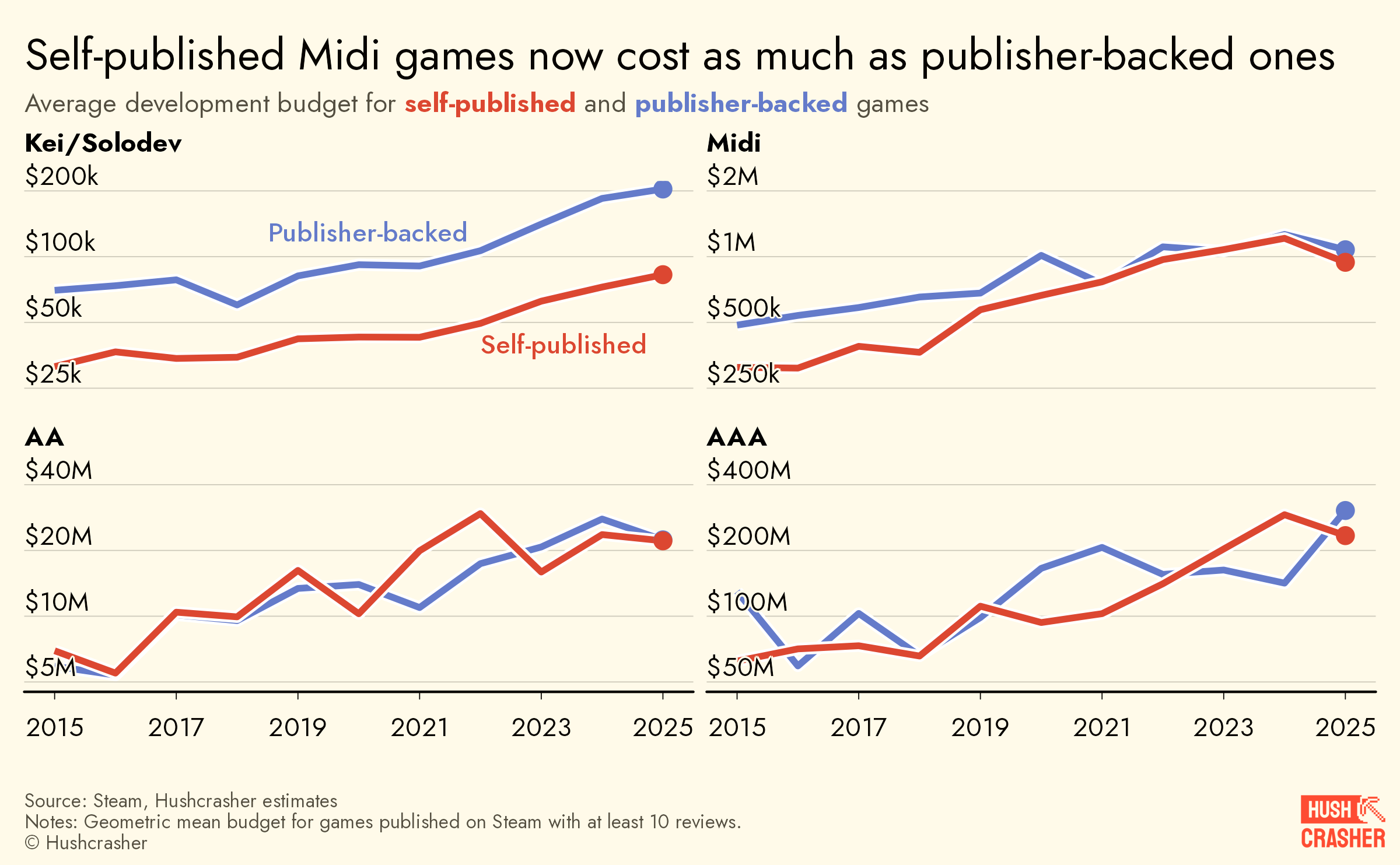

To be or not to be (self-published)?

Whether a game is backed by a publisher or self-published doesn’t only change who pays, it changes how much is spent. We’ve already touched on why here (principal-agent problem and all). But the picture gets a lot more interesting when you break it down by scope over time.

For Kei games, the publisher gap remains stubborn. A publisher-backed Kei game has roughly twice the budget of a fully independent production. This gap has remained particularly stable over time.

For Midi games, the picture is different. While there was a visible gap in the past, it closed around 2021. A decade ago, publisher-backed Midi games had budgets roughly 1.5 times higher than self-published counterparts.

Our best explanation so far is that above a given budget, the role of a publisher changes. For smaller scopes, signing with a publisher is transformative: it unlocks localization, QA, or more generally a boost in production value by letting the devs work longer on the project. Above a given threshold (we found it at around $500k), the difference between making it on a publisher’s money or yours starts blurring. Below it, the publisher adds ambition, above it, it “simply” makes the project feasible.

Meanwhile for AAA, the publisher question never mattered. The two curves have been tangled together for the entire decade. At this scale, the distinction is mostly artificial: most AAA studios are owned by their publisher anyway. Whether it’s CD Projekt shipping on its own dime, or Infinity Ward doing it under Activision doesn't make much of a difference.

So, budgets are going up. Across scopes, popular genres, and publishing models. If you felt that before, now you know it for a fact.

But “budgets are rising” is like saying “the patient has a fever.” Useful but not sufficient. What we want to know is: what’s causing it? We answered that here.

To the moon

One question remains: what will happen next? The waves of layoffs and AI adoption might suggest budgets are about to shrink. Our forecasts tell another story.

The end?

Forecasts up to 2027 and the ability to export each chart’s aggregated yearly data are reserved to paid subscribers. No budget for a subscription? Help us improve our benchmarks by sharing some insights about your released (or soon to be released) game and unlock 4 months of free access. We verify submissions within 24h, and all sensitive figures are strictly protected under NDA. Get started here.